CEAT Profit Plunge, Future Expansion

CEAT's Q1 FY27 Profit Collapses 96% Due to Rising Costs, Announces Expansion Plan

Anonymous

Key Points

1

CEAT has taken cumulative price increases totaling 5% to offset raw-material cost inflation driven by the West Asia crisis, with management describing these as calibrated to partly offsetting the impact while preserving demand and market share.

2

CEAT signalled an ongoing disciplined pricing approach for Q2, aiming to balance profitable growth with demand, as reiterated by management in post-results remarks.

3

A key margin pressure driver remains rising natural rubber costs, with market commentary noting rubber-cost inflation peaking around ₹267 per kg in June 2026, contributing to margin erosion.

4

CEAT’s Nagpur plant continues to be central to its expansion strategy, with plans to push capacity by about 53,000 tyres per day by FY31 and a focus on nearing full utilisation of current two-wheeler tyre capacity.

5

In Q1 FY27, CEAT’s consolidated EBITDA margin compressed to about 8.45% (8.5%), a sizable decline of roughly 615 basis points from the Q4 FY26 peak of 14.60%, underscoring persistent margin pressures despite double-digit revenue growth.

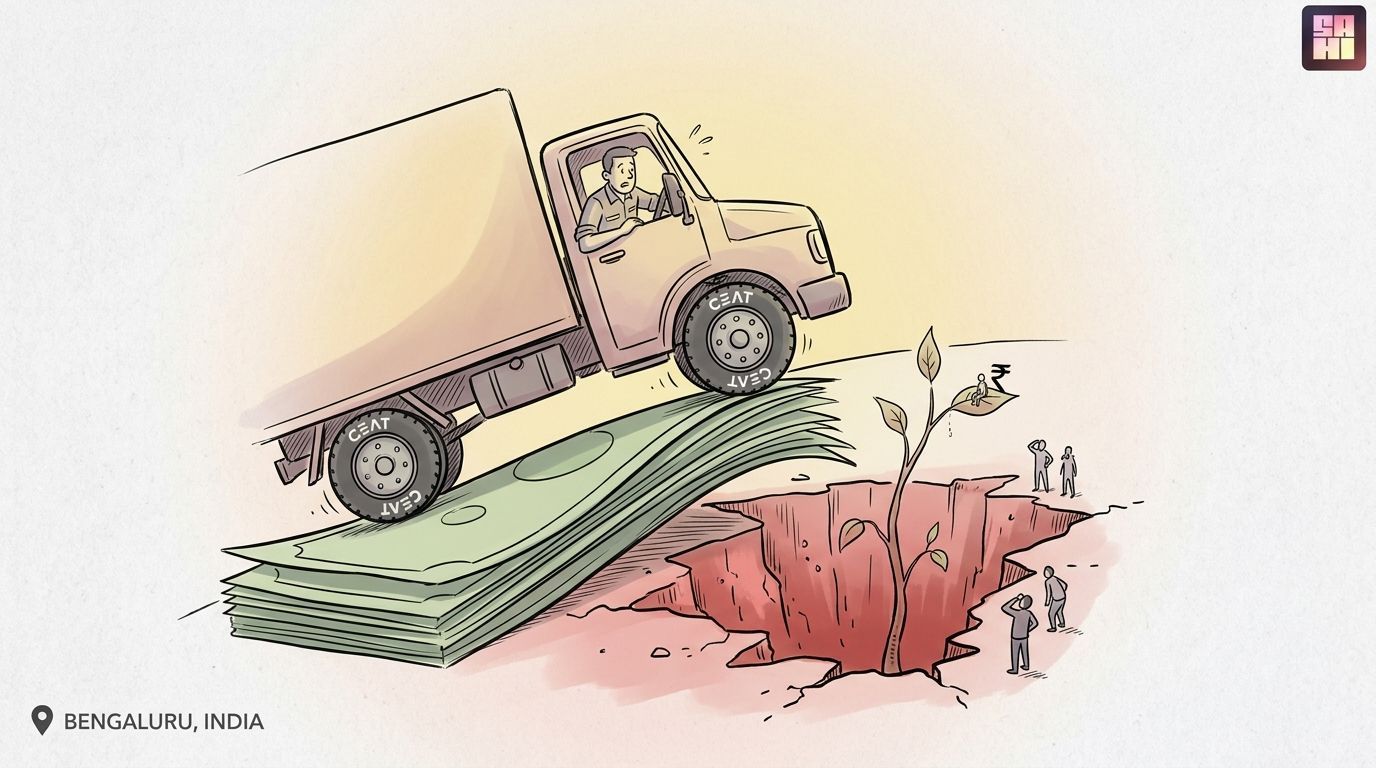

CEAT Limited posted a near-total collapse in quarterly profit, with net income crashing 96.4% year-on-year to just ₹4 crore in Q1 FY27, according to Whalesbook. Revenue told a different story — rising 22.4% to ₹4,318 crore — but surging raw-material costs swallowed almost all of the gains.

The Indian tyre maker's EBITDA — its core operating profit — fell to ₹365 crore, with margins compressing to roughly 8.5%. That is a steep drop from the 14.6% margin CEAT recorded just one quarter earlier, in Q4 FY26, as reported by Sahi.

Rubber Costs Hit ₹267 Per Kg, Crushing Margins

The main villain in CEAT's earnings story is natural rubber. Prices peaked at around ₹267 per kg in June 2026, according to Sahi. That spike drove raw-material costs sharply higher and squeezed margins across the quarter. EBITDA margins contracted by roughly 615 basis points from Q4 FY26 to Q1 FY27.

The West Asia crisis added further pressure by disrupting global commodity supply chains. CEAT's management described the resulting cost inflation as significant and ongoing. The gap between fast-rising costs and slower-moving selling prices left the company with almost no bottom-line profit despite strong revenue growth.

CEAT Raises Prices 5% but Keeps Demand in Mind

To fight back against cost inflation, CEAT took cumulative price increases totaling 5%, according to Whalesbook. Management called the moves "calibrated" — meaning they were designed to partly offset costs without scaring away customers or losing market share.

For Q2 FY27, management signalled a continued disciplined approach to pricing. The goal is to balance profitable growth with keeping demand healthy. CEAT has not passed on the full cost increase to buyers, which limits near-term profit recovery but protects its competitive position.

₹1,205 Crore Expansion Plan Targets 53,000 New Tyres Daily

Despite the profit pressure, CEAT is pushing ahead with a major capacity build-out. The company announced a ₹1,205 crore capital expenditure plan to add 53,000 tyres per day of production capacity by FY2031, as reported by Whalesbook. Funding will come from a mix of internal cash and debt.

CEAT's Nagpur plant sits at the centre of this expansion. Current capacity utilisation is running at about 95%, leaving little room to grow without new investment. The company is also focused on filling up its two-wheeler tyre capacity before pushing further into new segments.

Revenue Strength Offers a Silver Lining for the Long Term

The 22.4% jump in revenue to ₹4,318 crore shows that demand for CEAT tyres remains solid, according to Sahi. That top-line growth is the clearest sign that the company's market position is intact even as profits suffer. Volume momentum is real — the cost problem is what needs fixing.

If rubber prices ease from their June peak and CEAT's price increases take fuller effect, margins could recover in coming quarters. The ₹1,205 crore expansion also sets CEAT up for stronger output and scale by FY31. For now, though, investors face a company earning almost nothing on fast-growing sales.

Sentiment

Mostly NegativeNEGATIVENEUTRALPOSITIVE

Publishers

10

Articles

3

Reach

13

Topics

A

AnonymousAuthor