SME Digital Banking Surges

Revolut Business Leads SME Digital Banking Growth as Banks Innovate, Onboarding Remains a Challenge

Anonymous

Key Points

1

Revolut Business is signing up about 30,000 new companies each month, underscoring the rapid growth of its SME onboarding and its evolution into a broader operating platform for businesses.

2

HSBC’s 2025 SME push includes borrowing up to £100,000 for Small Business Banking customers and the open‑access Small Business Growth Programme developed with Microsoft, UpSkill Universe and Wired to provide technology, marketing and finance training (backed by Financing for Growth research and a branch network commitment).

3

UOB expanded its UOB Infinity ecosystem in 2025 by growing its anchor-company and supplier-spoke network to boost liquidity and procurement efficiency, with the platform’s ASEAN focus reflected by two-thirds of users based in ASEAN and availability across 10 markets.

4

Onboarding remains a major industry hurdle: about 70% of financial institutions report losing clients to slow onboarding, highlighting onboarding as the single most expensive architectural cost in scaling SMB and ISV services and the need for reusable, scalable onboarding architectures.

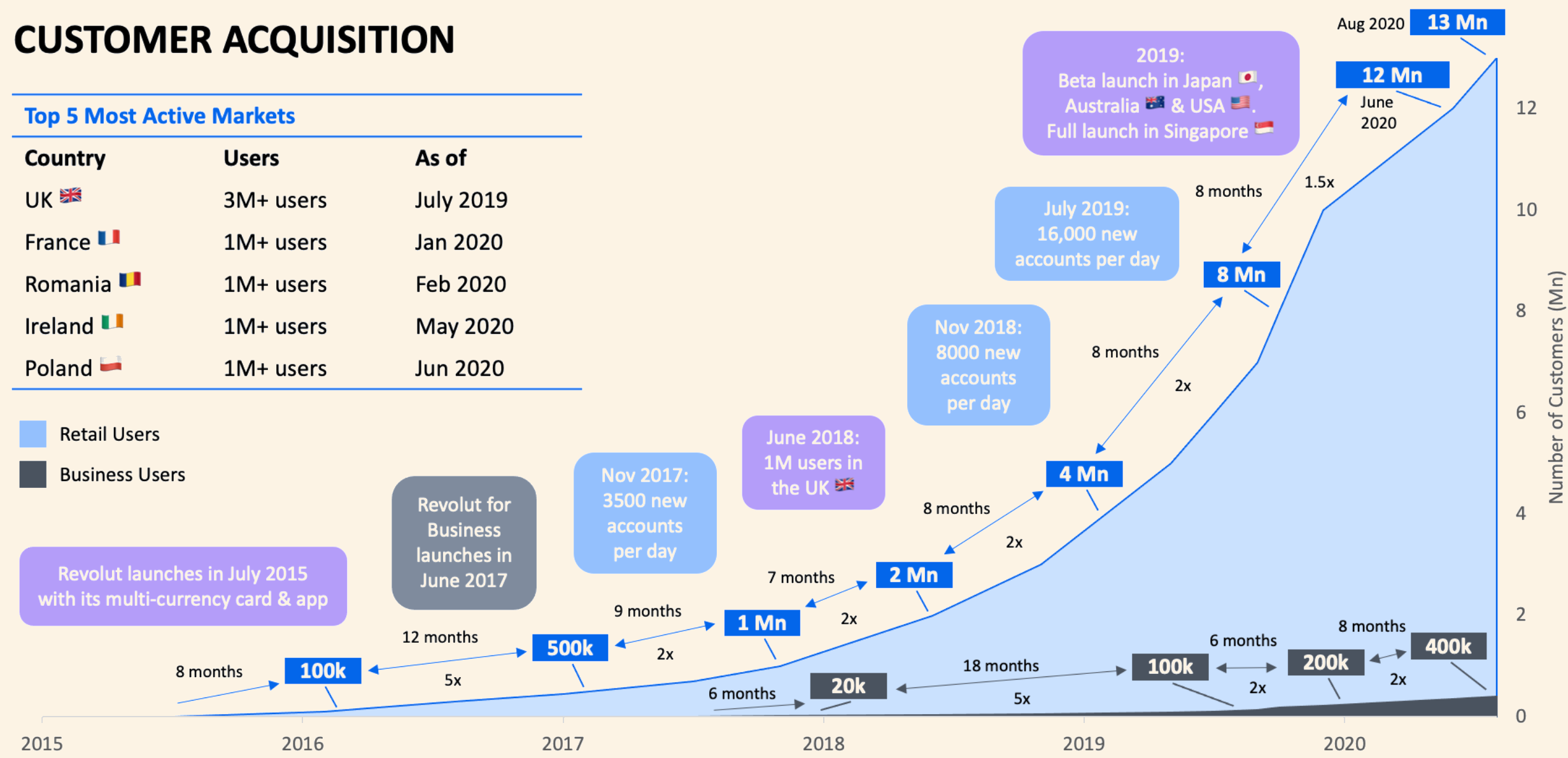

Revolut Business has grown to 767,000 business customers, signing up roughly 30,000 new companies every month, according to Euromoney. The unit now accounts for about 16% of Revolut's total income and processed $365 billion in 2025 — figures that have earned it the title of Europe's best digital bank for SMEs.

The result reflects a broader race among banks to win small and medium-sized businesses. From London to Tbilisi to Singapore, lenders are competing on speed, digital reach, and the depth of services they can offer growing companies.

Revolut Turns Fast Onboarding Into a Full Business Platform

Revolut did not stop at quick account opening and multicurrency cards. It pivoted to become what it calls an operating platform for businesses. That shift — from onboarding tool to daily business hub — drove a 33% jump in business customers in 2025, Euromoney reported.

The growth is hard to ignore. Thirty thousand new companies join each month. At $365 billion processed last year, the business unit is no longer a side project. It is a core revenue driver, generating roughly one in six dollars of the group's total income.

HSBC Cuts Fees and Pledges £5 Billion to Win UK Small Businesses

HSBC took a different approach. The bank removed the monthly fee on its Small Business Banking Account, giving customers free UK digital banking and access to business specialists. It also promised £5 billion in SME lending over five years, according to Euromoney.

HSBC also launched the Small Business Growth Programme, built with Microsoft, UpSkill Universe, and Wired. The program offers free training in technology, marketing, and finance. Small Business Banking customers can borrow up to £100,000. HSBC kept its branch network open through 2027 to help owners with bigger financing decisions.

Bank of Georgia Processes 98.79% of SME Transactions Digitally

In Central and Eastern Europe, Bank of Georgia set a remarkable benchmark. In 2025, 98.79% of SME banking transactions went through digital channels with no branch involved, Euromoney reported. That figure earned the bank the title of CEE's best digital bank for SMEs.

The result shows how far digital adoption has gone in a region not always associated with fintech leadership. For SME customers, it means faster service and lower friction — without ever walking into a branch.

Slow Onboarding Still Costs Banks Millions of SME Customers

Despite all this progress, one problem persists across the industry. About 70% of financial institutions report losing clients because onboarding is too slow. That makes onboarding the single most expensive architectural cost in scaling services for small businesses and independent software vendors.

The solution most banks are chasing is reusable, scalable onboarding systems — built once, deployed across many products. UOB is doing this through its UOB Infinity platform, now live across 10 ASEAN markets, with two-thirds of its users based in the region. Speed of entry matters: UOB even created a Green Lane program to help businesses get into new markets faster.

Sentiment

Mostly PositiveNEGATIVENEUTRALPOSITIVE

Publishers

10

Articles

0

Reach

10

Topics

A

AnonymousAuthor